Simran Alchemist

February 11, 2021

Aluminium is the most available metal on the earth crust and is widely used due to its inherent properties and its recycling nature. It has got high use in automobile, packaging, aerospace, electrical to name a few. With the rise in demand of the material from automobile sector and the OEM sector it has gained its momentum in market dynamics.

Global Aluminium market size in 2019-2020 was USD 172 billion and expected to reach USD 250 billion by year 2026-2027, exhibiting an approximate CAGR growth of 5.2%. However, Aluminium is used by automotive sectors though ages but with the rising call for introduction of the Electrical vehicles, the demand would rise multiple times owing to the light and sturdy property of the material.

Alumunium alloys used in different segments of the component manufacturing of machine parts will replace Stainless steel due to the rising cost of the stainless steel . Globally, recycling of Aluminium is being adopted due to 100% recyclable ability with minimal power consumption.

India consumes primary aluminium to approx. 2.1 million MT as per annum in 2019. India imported Aluminium Scrap approx. 14 lakh metric tons.

India’s per capita consumption of aluminium stands too low (~ 2.5 kg) compared to China (24 kg) and world average (11kg).

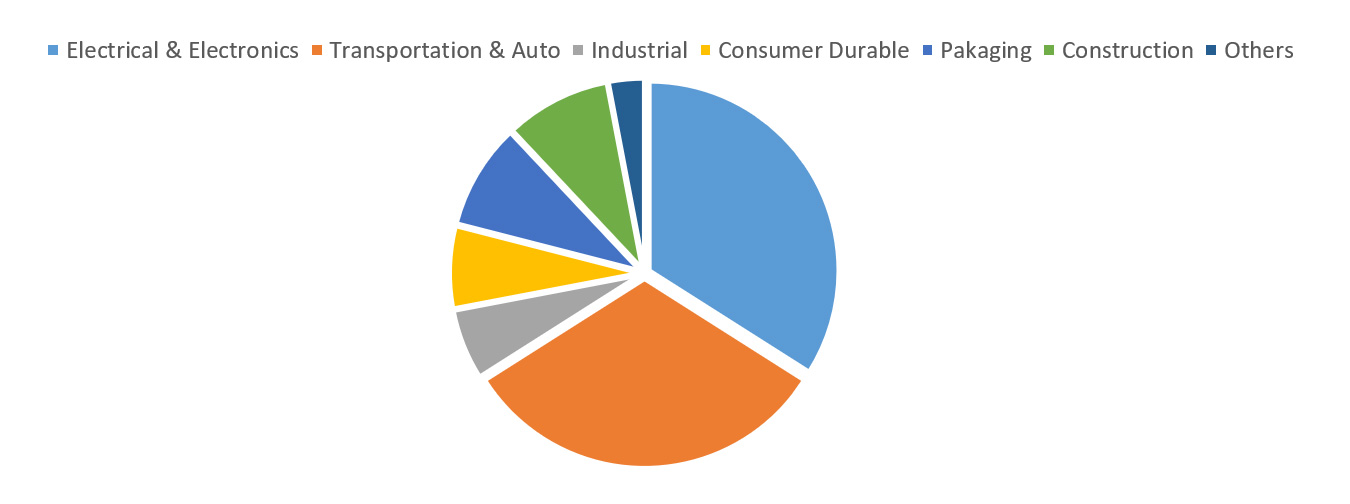

The main primary aluminium consuming sectors, as of 2018, include electrical sector (38%), transport sector (34%), construction (9%), consumer durables (7%), machinery & equipment (6%), packaging (2%) and others (4%).

Aluminium products can be manufactured using a combination of both primary and secondary aluminium depending on the specification of the final product.

Secondary aluminium producers who account for about 37 % of aluminium consumption in India.

There are more than 250 players in the unorganised secondary aluminium sector with recycling consisting of numerous SMEs spread across various states in India.

Castings account for about 70% of the recycled aluminium usage in India; Billets, re-rolling units and steel de-ox make up the balance 30%.

Transportation (mainly automobiles), followed by building & construction, consumer durable products and other industrial applications are the major users for recycled aluminium in India. The market for recycled aluminium in India has been growing at around 10% per annum during the last few years.

Typical Aluminum usage in India:

Analysis & Trends:

With steep upward movement of the prices in global market, the price correction is expected. The aluminium market may dive its nose to downward direction, with LME futures falling toward the $1,960 region amid a high level of inventories in LME and Shanghai-bonded warehouses. Such global correction may also induce the Indian Aluminium major- NALCO to revise its prices from 170 per kg prevailing.

Forecast Ahead & Conclusion :

Aluminium is expected to trade at USD 1950 per Ton by the end of this quarter of this FY at LME. With the new policy announced of vehicle scrappage in India, the demand of the aluminium and its alloys is expected to rise in days ahead and the Indian Aluminium Market is expected to remain strong bound.

Simran Alchemist

September 17, 2020

Market insight and its effect on Aluminium and Cement Industry

Facts:

1. India is the world’s biggest consumer of pet coke.

2. Local producers include Indian Oil Corp, Reliance Industries and Bharat Petroleum Corp.

3. It is dark solid carbon material. Cement companies in India account for about three-fourths of country’s pet coke use.

4. Usage of pet coke in energy-hungry India recently had come under scrutiny due to rising pollution levels in major cities.

5. Import of pet coke is allowed for only cement, lime kiln, calcium carbide and gasification industries, when used as the feedstock or in the manufacturing process on actual user condition.

Market Insight:

Calcined petroleum coke (CPC) market will witness growth on account of its low emission properties coupled with soaring investments toward the development & expansion of the primary metal manufacturing industry. Increasing utilization of calcined petcoke as a recarburizing agent along with its growing demand across the steel mills will enhance the industry outlook. Moreover, shifting trend toward use of coke as a substitute of coal in furnaces & boilers will positively influence its adoption over the forecast timeline.

Fuel petcoke industry is set to witness gains on account of ongoing investments toward expansion of cement manufacturing capacities and development of thermal power plants. Low ash content and high heat & gross calorific value are some of the key features that favour the adoption of fuel grade petcoke over other available alternatives.

Petroleum coke market from aluminium industry is set to witness substantial growth by 2024. High ductility, anti-corrosion property, light weight and excellent thermal & electrical conductivity are some of the key underlying properties of aluminium which makes it suitable for key industries including medical, electrical components and ceramics. In addition, rapid urbanization across emerging economies has created an incremental demand for the metal, which will drive the business growth over the forecast timeframe.

Petcoke demand across power plants will witness growth owing to increasing adoption of fuel with high energy content along with the growing demand for electricity across emerging economies. High fuel stability and less risk of combustion during transportation are some of the prominent factors favouring the product adoption.

Demand for petcoke across Asia-Pacific is anticipated to witness robust growth on account of growing demand for cement to support ongoing expansion of urban centres and development of public infrastructure. Surging investments toward the development of new commercial and industrial facilities coupled with growing measures to reduce the dependency on fossil fuels including coal will further propel the product adoption.

Eminent players: Saudi Aramco, BP, Essar Oil, Reliance Industries, Chevron Corporation, Valero Energy Corporation, Indian Oil Corporation, Trammo, Marathon Petroleum, Oxbow Corporation, Aminco Resources, HPCL-Mittal Energy Limited (HMEL), Bharat Petroleum, Shamokin Carbons, Rain CII, Cocan Graphite, Atha Group.

Conclusion:

Low-sulphur anode grade petroleum coke prices are very weak.

Anode grade GPC and CPC prices have fallen faster than Aluminium prices as some merchant calciners have struggled with the impact of changes in Indian regulations.

The cement industry should benefit from lower crude prices, as pet coke prices decline. Freight costs, too, can be expected to reduce, which can aid margins of cement companies.

One of the biggest beneficiaries of lower crude prices could be paint companies, as a big share of their raw materials are crude-linked.

Simran Alchemist

May 18, 2020

The logistics industry is working hard to catch up with demand and supply that’s being affected by COVID-19. But with the spread of this deadly virus, almost every industry, everywhere, is now being affected. Whether it’s raw inbound goods, a manufacturing level, a distribution level, everybody’s experiencing a pain point somewhere in their supply chain.

It is pragmatic that around 65-70% of loaded vehicles are stranded on roads near the Naka / State borders due to imposed lockdown. Transporters are trying their best to de-stuff the critical goods of their clients to their nearest warehouse / godown but facing problem as labours are not available to unload these goods.

The situation is less critical for cargo movement that occur within a given state, while inter-state movements remain more challenging due to a big drop in Imports from other countries. Intra-movement of goods are also limited as drivers are reluctant to operate on roads due to challenges in getting basic needs enroute. Some drivers have taken Holi leave but not yet reinstated due to fear of contagion.

The most affected areas are Seaports. Vessels are quarantined and not allowed to board at near ports Containers are stuck up at ports due to lack of labours, drivers & trailers. CHA/FF activities are hampered due to unavailability of government & port authorities. Inter-plant or short distance transport movement of raw materials is bit limited due to manpower issues. Many plants are shutting their operations due to limited raw materials, scarcity of labours and safety of workers.

Transporters are working diligently on the safety of their employees while working to mitigate any potential impact on the supply chains and operations of their customers. Transporters are currently working from office with only 30-35 % capacity by imposing limited working hours. The front office staff such as loading supervisors, drivers and operations managers have been provided with the face masks, hand sanitizers and are regularly being monitored for cold. Safety measures are already being followed carefully at facilities, truck stops, and on loads that are traveling across the country.

The transportation world will surely find a way once lockdown is called off but there may just be some delays along the road. Freight rates are expected to increase by 5-8% post lockdown due to high demand across different industries. The vehicle scarcity is not expected but many vehicles will not be operational due to delay in driver comeback. The overall logistics industry will take at least 2-3 months to retain to regularization.

Simran Alchemist

January 30, 2020

Time to Grab on the Raw material- FerroVanadium

Understanding Vanadium

Steel is among one of the pillars upon which economy of any country withstand. It has been more than a year now steel market has witnessed a downtrend and the imbalance of demand and supply has emerged a fall in economies of developed countries. Trade war between US and China has further fueled up the situation and recovery from downtrend has been stretched.

Down the chain, the raw material market associated with steel making has also seen a fall in the demand. The economies of fast developing countries like India, the GDP has restricted to 4.8% which was projected to be above 7%.

Noble metals has been sold worldwide at premium prices due to rising demand in the US and Europe markets and manufacturers from China benefitted by exporting to the west countries. Now, with the less demand and fall in specialised steel production, the offtake of the noble metals has fallen sharply.

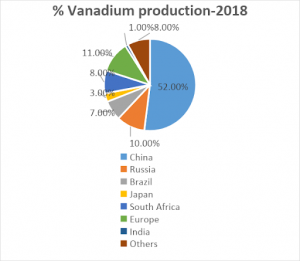

Vanadium alloy productions is segmented on the basis of alloy produced. Ferrovanadium, Nitrovan, Nitride vanadium. Ferrovanadium vanadium accounts for 92% share as per 2018 productions which makes the largest market of vanadium alloy across the world.

Domestic Trends:

Vanadium is one of the element that is mostly used in steel industry and it accounts 90% of global consumption. Ferro Vanadium(FeV) of 80% and 50% grade are mostly use in manufacturing of specialised steel in India. India steelmakers consume ferrovanadium approximately 2800 metric tonnes annually. The current year , the consumption has fallen by almost 40% from the annual trends.

Analysis: Past and Present

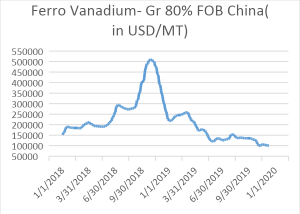

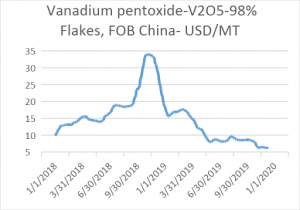

Imports from Checz republic for 80% grade FeV done at an average price of USD 22.90 per kg- Basic ( INR-2060 per kg )- CIF Mumbai port in October-19.

If we analyse the global market the major cost driver that accounts the cost of ferrovanadium production shows a fall in the Raw material cost ( vanadium pentoxide-V2O5) in the major markets- Rotterdam – Europe and China. In last one year the prices of V2O5 has fallen by 39.78% and 38% respectively in Europe and China Markets.

Around a year and half back, the prices of FeV was at its highest levels and availability of V2O5 was limited, immediate orders was sold at a premium rates with deliveries uneven. Companies who had their own resources gained from the market situation and clinched the orders. Small and medium size companies has to gather V2O5 slag and then comply the small orders.

Presently in China market V2O5 is sold at the rate of 96000 RMB/ton plus taxes , which is up by 500RMB/ ton from last week prices.

Due to the trade war with US and China, China is not piling up the stocks and maintaining the price levels . For a 6 months delivery the offered prices are at the range of 98000 to 99000 RMB/ton and applicable taxes.

International and Indian producers( FeV):

International: ( Top3)

Bushveld Mineral Limited

Tremond Metal Corporation

Bear Metallurgical Company

Indian: (Top 3)

Essel Mining

Premier alloys

Rover ferroalloys

Future Outlook & Trends :

Globally FeV alloy market is expected to attain a value of USD 5800 Million by the end of 2025( INR 4175 Crores) from USD 3,850 Million in 2018( INR 2772 Crores). This growth is at the rate of 5.5% CAGR for the period of 2018-2025 due to increase demand in steel for infrastructural development. US markets is expected to grow at 5% YOY and China is expected to grow at 8.5% YOY for next 3 years.

What to benefit:

Prevailing low prices and the outlook of stable prices for next 6 months timeline is most likely benefit the Indian steel manufacturers. Immediate price escalation is least expected even at the global level. With low orders in hand among the Indian and international alloy manufacturers , it is an even better opportunity to get the online negotiated price for a longer delivery period to grab the maximum benefits.

It is estimated that for 50% FeV supplies and for 80% FeV supplies, the prices from Indian manufacturers would see at a level of INR 965 per kg and INR 2015 per kg respectively.

Recommendation:

Indian steel makers should exploit this opportunity in booking the materials with forward 6 months deliveries through the online competitive price discovery .

Mjunction which has years of experience in procuring FeV for their leading clients ,procuring approx. 1000 MT of 50% grade per annum FeV benefitting approx. savings of 10-12% savings from clients estimates.

Simran Alchemist

November 29, 2019

The Plastic usage in India has been increasingly under scanner, because of visible pollution created by uncollected post-consumer waste. The backlash has been aggravated by global anti-plastic sentiments, resulting in rapid consumption of plastic mainly for packaging which provides functionality for a short time before it becomes waste and ends up in landfills and oceans affecting the ecosystem. The anti-plastic tsunami has resulted in the prologue of strict regulations by State and Central Government. This new law has banned several single-use plastic products, to tackle the issue of post-consumer plastic waste. This has resulted in sourcing solutions for large corporate on what should be used as an alternative to plastic.

List of banned items:

1. Less than 200 ml of drinking water PET bottles

2. Plastic Mineral water pouch

3. Plastic bags (with/without handle)

4. One time use / Single-use disposable items made up of thermocol or plastic

5. Disposable dish/bowl used for packaging foods in hotels and straw

6. Use of plastic and thermocol for decorative packaging

To achieve the environmental goal of reducing plastic pollution, various solutions are being recommended by industry experts. With the changing law, various products have emerged which have reduced cost in procurement.

Below are a few recommendations on how to reduce plastic pollution-

Stopping single-use Plastics packaging:

Phasing out and banning of specific products/ groups of products is being considered. This step is a big part of the business. e.g.

• Convenience for user

• Social Impact

• Commercial impact

• Consumer Preference and affordability

Environment Regulations:

Government regulations are being imposed on the usage of plastic. Such regulations demand the plastic using industry to invest actively in:

• Adequate infrastructure facilities for proper waste management.

• Ensuring effective implementation of Regulatory guidelines

• Conducting various awareness programs to educate the members regarding environmental compliance.

• Setting up direction to help them fulfill their environmental legislation.

Recycling:

This is the most effective solution. But at the same time, this needs a high level of self-discipline & planning:

• Recycling facility management.

• Land for setting up Recycling Facility.

• Funding to encourage recycling.

• To develop a better collection mechanism.

• Promote various recycling programs and workshops.

• Conduct awareness programs for waste minimization, resource optimization etc.

These new restrictions and regulations are increasingly being enforced.

To serve this purpose, our procurement professionals have come up with an alternative packaging solution. With that, we have minimized the use of plastic and now our alternative packing solution is jute. It is extremely sturdy and is highly durable, it is 100% biodegradable, and is easily recyclable. It also causes no harm to the environment. We believe that it is our duty to protect our environment and a small step can also make a huge difference to save our planet. Our consultants in the field of purchase, supply chain & packaging are already geared up to support the industry towards quick & cost-effective adoption of alternative packaging.

Also, this will help to reduce cost in procurement & alternate materials sourcing and substitution.

Simran Alchemist

October 30, 2019

Artificial Intelligence does not need any introduction these days as we are in an era where it is going to take the centre stage. Machine Learning is going to be applied in calculative planning, sourcing & supply management of MRO items for large manufacturing organization. But first let’s figure out major challenges that, we as a procurement professional face in sourcing MRO items through conventional route –

• Substantial spend, spread across multiple plant/sites and categories

• Numerous unique SKUs, many of which are used only on certain equipment

• Unpredictable demand ― some 70% of MRO items turn less than once every two years

• A “just in case” mind frame, buying more than actually needed

• Large number of vendors, including local vendors at individual sites

• Spot buys ― unplanned purchases accounting for 50 percent of total MRO spend

All these factors lead companies to overstock, which when done again & again result in obsolescence. Technology in our era have contributed enormously & Machine Learning is one such solution which is ready to handle such issues meaningfully. It is prepared to address & eradicate major constraints for MRO category right from the source.

The ITES & eCommerce platform based companies are making strong associations with AI and machine learning. This AIML suites are looking to solve all existing problem with MRO category management with the help of data. Such IT enables take inputs from a wide variety of sensors, past maintenance data & schedules to accurately predict a breakdown and need of spares so that company can provide a preventive solution beforehand. Preventive maintenance will help organizations not to lose out due to down time of production. At the same time a greater safety stock need not be maintained as everything will fall in more or less planned schedule. It will save us from unnecessary inventory carrying cost & overstocking mind-set. Spot buying, in most of the time, will be enough to keep the plant in operational condition. This AIML looks to simplify the work of the procurement professionals in the future, with the smooth flow of operations and optimizing spends in MRO procurement. Together with, downtime improvement and gain in inclusive efficiency.

The future of MRO procurement lies not only in predictive maintenance but also in the ability to automate purchases & supply chain. Procurement teams will always be available with data on stocks and inventory, combining this data with predictive maintenance data, The IT suite can ascertain if a specific part’s stock needs to be replenished or not.

A syndicate between ML & AI would support in administering text search operation across gambit of unclassified data of the tail end voluminous MRO stocks to also predict near matches while the need arises for a specific item. This AIML combined search operations are generally more efficient as compared to predefined text base sear engines.

Once it signals for procurement of any item, The IT systems can handle the entire process, starting from need identification to supplier verification, getting quotations, analysing quotes to placing contract. The entire purchase cycle is in the realm of AIML automation enabled by a robust database where codification of item/parts are perfect for retrieving an outcome that is derived is a full proof solution.

Now, when it comes to automobile/engineering industry, a combination of integrated logistics & AIML driven procurement systems would eliminate the obvious possibility of generating obsolescence, when the safety stock can be reduced to a greater extend. AIML is likely to help the profit & variety trodden Automobile industry in reducing possible obsolescence & thus help on profitability.